THE GAP. Part I: Unseen.

There are two healthcare systems in America. One for Congress. One for everyone else. Here's what the numbers actually show.

There is a version of the American healthcare debate you already know.

The one where both sides argue about coverage while premiums rise. The one where politicians hold hearings, give speeches, and fly home to their taxpayer-subsidized health plans. The one where insurance company CEOs collect eight-figure paychecks while the people paying their premiums skip appointments, ration medication, and hope nothing serious happens before they can figure out the math.

That version is not wrong.

But it is incomplete.

The part that has been left out is simpler and more devastating than anything being argued on cable news right now. The system is not broken. It is working exactly as designed. The question nobody is asking is — designed for whom?

The insurance industry spent $183 million lobbying Congress in 2024. That is your answer.

He Made a List.

A friend called me Friday. Someone I’ve known since my twenties. He has spent his career in hospitality — the industry that feeds us, celebrates us, marks every milestone worth remembering. The kind of person who knows your name, your story, your drink order from three years ago. The kind who makes everyone in the room feel like the most important person there.

He called to say goodbye.

Before the MRI results. Before the priest. Before the machines and the beeping — he had a list. The people who mattered most.

I made the list.

For the past month, he had been rationing his medication. Not because he wanted to. Because he had to.

When you have had an organ transplant, the anti-rejection medications are not optional. They are the difference between your body accepting what kept you alive and your body destroying it. One medication alone runs over $500 a month out of pocket. On top of premiums. On top of everything else a person navigates when no employer is picking up any part of the tab — and when small businesses can barely afford to offer coverage even if they want to.

In this country, Amazon receives billions in tax incentives to expand. The person building something from nothing gets a premium bill they cannot afford.

So he made choices. Quietly. Without telling anyone. Putting on the tough exterior that gets you through the day while something slowly goes wrong underneath.

My heart broke when I found out. Because I didn’t know. And that is exactly how the system counts on it working. People suffer alone because suffering out loud feels like failure. By the time anyone finds out, it is often too late.

The Gap Has a Body Count.

Last August I got pneumonia again. My second time in a few months. When you have had more than half of a lung removed, pneumonia is not something you push aside casually. It landed me in the hospital.

What I thought was a sinus infection turned out to be a raging infection that had moved into the bone in my skull. Mastoiditis. I ended up in the emergency room. Five rounds of heavy antibiotics later, I am still navigating the aftermath. My doctors have ordered a specialized brain MRI.

I have been waiting three months.

Not because I don’t know better. Not because I stopped fighting. Not because my head stopped throbbing.

Because the cost is $3,000 out of pocket and the system has no answer for someone like me.

And I cannot access the imaging I need to find out if the infection is improving or whether we need to consider additional measures.

That is not a personal failure. That is the gap.

Before anyone suggests socialized medicine is the answer — I have been on a waitlist as an “urgent” case to see a neuro-ophthalmologist for five months. Five months. Urgent. The problem is not simply who pays. The problem is any system — public or private — that calls something urgent and then makes you wait half a year.

There are really only a handful of paths forward:

Universal coverage — with all the wait lists that come with it.

True market competition — eliminating state lines, letting companies compete nationwide, forcing the math to actually work.

Eliminate the fraud and corruption — bleeding the system dry before anyone sees a dime of actual care.

None of these are easy. All of them are better than what we have now. That is where Part III goes.

But first — the numbers.

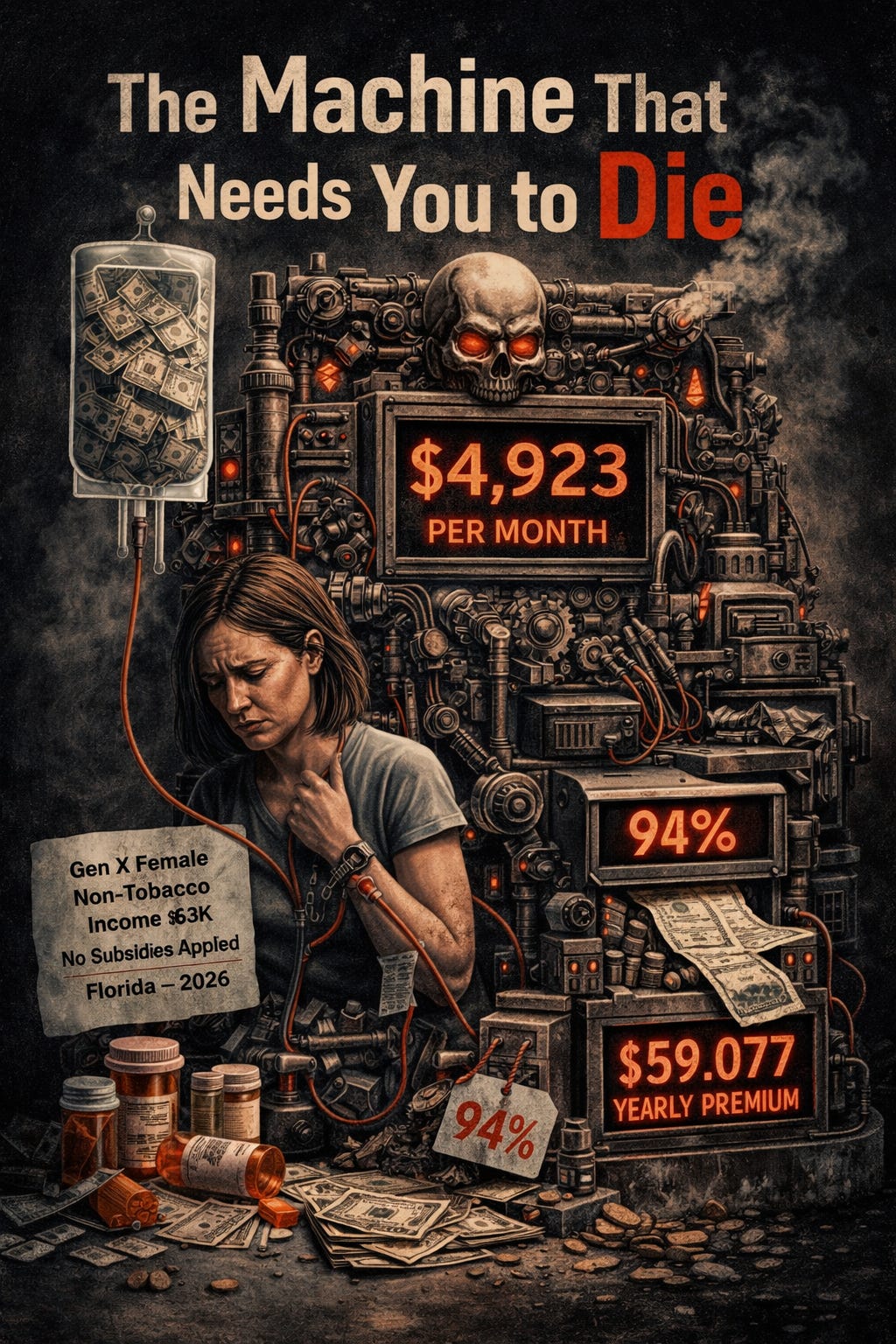

The Machine That Needs You to Die.

Gen X Female. Non-tobacco. $63,000 annual income. No subsidies applied. Real search on stridehealth.com. March 2026.

I focused on PPO plans — because when you are navigating serious medical needs, a PPO is not a luxury. It is the plan that gives you access to the specialists and hospitals you actually need. HMOs restrict your network. When your health is on the line, network restrictions can cost you your life.

Someone will say: there are cheaper plans. And they are right.

But an HMO restricts your network. When you are managing a transplant, a bone infection, a neurological condition, a cancer diagnosis — your network is not a preference. It is the difference between seeing the specialist who knows your case and starting over with whoever happens to be in-network this month. PPO coverage is not a luxury for people with serious medical needs. It is the minimum viable option.

And even the cheapest HMO Gold plan in Florida for a 63-year-old runs nearly $1,900 a month. That is $22,800 a year. For someone earning $63,000 gross — before taxes — that is 36% of their income. Just for the premium. Before a single claim.

The cheaper plan doesn’t make the argument disappear. It just moves the number.

Now look at what age does to the math. Real searches. Same zip code. Same income. Same plan tier. Ten years apart.

Florida — PPO — Female — Non-Tobacco — $63,000 — Unsubsidized:

Age 52 (born 1973)

Gold PPO: $2,505/month — $30,065/year — Max OOP: $6,250

Platinum PPO: $3,255/month — $39,064/year — Max OOP: $2,525

Age 63 (born 1962)

Gold PPO: $3,788/month — $45,467/year — Max OOP: $6,250

Platinum PPO: $4,923/month — $59,077/year — Max OOP: $2,525

Under the ACA, insurers can charge older enrollees up to three times what they charge younger ones. In Florida, they are charging close to that ceiling.

At age 63 — one year from Medicare — a woman earning $63,000 a year is quoted $4,923 a month for Platinum PPO coverage.

That is $59,077 a year. Her entire gross income is $63,000. The premium alone consumes 94% of it. She has $3,923 left for the year. For everything else. Food. Rent. Utilities. Medication. Life.

And the Max Out of Pocket column. One hospitalization. One emergency room visit. One serious diagnosis. She owes another $2,525 on top of every premium and copay already paid.

Now look at Washington DC — where Congress lives and works.

Washington DC vs. Florida — Platinum PPO — Same Person — Same Income:

DC, age 52: $1,458/month — $17,518/year — Max OOP: $2,100

Florida, age 52: $3,255/month — $39,064/year — Max OOP: $2,525

Florida, age 63: $4,923/month — $59,077/year — Max OOP: $2,525

Members of Congress do not pay the DC rate either. Taxpayers cover 72 to 75% of their premium. A member of Congress pays roughly $365 a month for Platinum-level coverage.

$365 a month. While a 63-year-old woman in Florida is quoted $4,923.

We are not asking for a handout. We are asking for what Congress has. Or put them on the same system the rest of us navigate. Let them open stridehealth.com with their own money. Let them feel the table.

And while we are at it — every elected official should earn the median income of the state they represent. They should live inside the same healthcare system they legislate. And when their term ends, so does the taxpayer-funded salary. The rest of us build without a safety net. We show up. We grind. We do the impossible in spite of every obstacle the system puts in our way. That is what resilience actually looks like.

Two Women. Two Systems. Only One of Them Is Working.

Yesterday, the White House announced that Chief of Staff Susie Wiles has been diagnosed with early-stage breast cancer — caught early, with an excellent prognosis.

I have had the privilege of working with Susie. She is one of the most accomplished women in American political history — and in January 2025, she became the first woman ever to serve as White House Chief of Staff.

And I am deeply grateful she has access to the world-class care she deserves — the White House Medical Unit, Walter Reed, Bethesda Naval, and federal employee health benefits covered largely by American taxpayers.

She deserves every resource available to her.

And that is exactly the point.

There are not one but two healthcare systems in this country:

System One: Federal employees and elected officials. Insulated from the market. Subsidized by taxpayers. Designed to work. When something is caught early, it gets treated immediately.

System Two: Everyone else. Exposed to every compounding failure documented above. When something needs imaging, you wait three months because the cost is out of reach.

The people running System Two have never lived inside it. That is not an accusation. That is the structural reality. You cannot feel what you cannot see.

Somewhere in America today, someone is rationing medication they cannot afford. Somewhere, a person is waiting three months for imaging their doctor ordered. Somewhere, a woman is deciding whether the mammogram is worth the out-of-pocket cost this month.

The difference between those stories is not character. It is not effort. It is not how hard someone worked or how much they deserve care.

It is a zip code and a job title.

370 Times.

The six largest health insurance company CEOs took home a combined $159.4 million in 2024.

Andrew Witty — UnitedHealth Group — $26.4 million — 348x the median employee salary

Gail Boudreaux — Elevance Health — $20.5 million — 370x the median employee salary

David Cordani — Cigna — $23.3 million — 279x the median employee salary

David Joyner — CVS Health / Aetna — $18.2 million — 299x the median employee salary

Source: Becker’s Payer Issues, SEC proxy filings, April 2025

370 times the median employee salary. For the CEO of the company deciding what gets covered and what gets denied.

The insurance industry spent $183 million lobbying the people who write the rules in 2024. Not to fix the system. To keep it exactly where it is.

That is not a broken system. That is a system working perfectly for the people who built it.

The Subsidies Were Never the Fix.

We did not arrive here because of one administration. This has been decades in the making — multiple presidents, both parties, administration after administration that chose the path of least resistance while the lobbying dollars piled up and the costs quietly compounded.

The enhanced ACA subsidies were not a fix. They were a bandaid. They masked an artificially inflated cost structure while insurance company executive teams collected hundreds of millions and rates kept climbing underneath.

When the bandaid was ripped off at the end of 2025, two things hit at once:

The real unsubsidized price surfaced.

Years of compounding rate increases — that never stopped — arrived simultaneously.

Premiums jumped 21% in a single year. That is not a coincidence. That is the bill coming due.

And it landed squarely on small business America and independent contractors — the people with no employer, no union, no government program standing between them and the full weight of a market that was never designed to work for them.

What happens next will determine whether small businesses and contractors can survive in spite of this. That is not an exaggeration. That is the math.

Eighty percent of this country voted for accountability. For the fraud and corruption to end. For a government that works for the people funding it. We want to provide for our families. We want the system to make sense.

We are still waiting.

$317 Billion Out. Zero Coverage In.

The United States is the only wealthy nation on earth that does not guarantee healthcare coverage to its citizens. Every other country in the G7 — Canada, France, Germany, Italy, Japan, the United Kingdom — has found a way to cover its people.

We write the checks that fund the world.

In FY 2024, the United States sent foreign aid to 179 countries. Here are the top recipients — and what they provide their own citizens:

Top US Foreign Aid Recipients — FY2024 — and Their Healthcare Systems:

Israel — $6.82 billion — Universal coverage. No deductibles. Funded by national income tax.

Ukraine — $6.5 billion — Universal coverage system.

Jordan — $1.75 billion — National health insurance. Majority of citizens covered.

Egypt — $1.5 billion — Government-subsidized healthcare for citizens.

Source: USAFacts, ForeignAssistance.gov, Commonwealth Fund, FY2024

Since 1951, the United States has provided over $317 billion in inflation-adjusted aid to Israel alone. We are not suggesting these countries don’t deserve support. Strategic alliances matter. We understand that.

We are asking one simple question: why is the country writing the checks unable to cover its own people?

We just want what members of Congress have. Or put them on the same system we navigate. Let them open stridehealth.com and run the same search. Let them feel the table.

We are not asking for a perfect system. Every system has tradeoffs. But right now we have the worst of every option — the cost of a market system without the competition, the complexity of a government system without the coverage, and the fraud of both running underneath it all unchecked.

Go South, They Said.

People are leaving New York, New Jersey, California — drawn by the promise of lower taxes and a perceived better financial picture. The tax savings are real for some people.

But before you pack the truck, run the full number.

Health insurance in Florida runs significantly higher than most states — the numbers above prove it. Homeowners insurance has become nearly unaffordable in many areas. Car insurance. Flood insurance. The cost of staying insured in Florida across every category is not what the headline tax savings suggest.

Here is something I did not expect to say: my cost of living in DC was technically lower than what I am navigating in Florida right now.

Not because Florida is expensive in the ways people think. Because the systems nobody talks about — healthcare, homeowners insurance, car insurance, flood insurance — compound in ways that don’t show up in the tax savings headline.

Before you move: if you are self-employed, between 45 and 64, or navigating any kind of health situation — model the full picture. What you save in taxes may not cover what you lose in insurance costs.

These are the cracks that reveal how broken so many systems truly are.

The Search Takes Four Minutes. Run It.

This series does not end with outrage and no direction. That is not how I am built.

Run your own numbers. Go to stridehealth.com. Enter your zip code, your age, and your actual income with no subsidies applied. Screenshot what comes up. Then enter 20001 — Capitol Hill. Screenshot that too. Look at both. Share both. That is the story.

Call someone. Not a text. A call. If there is a person in your life you have been meaning to check on — do it today. You do not know what list you might be on.

Ask twice. The first answer is almost always “I’m fine.” Ask again.

Know your full number. Write down what healthcare is actually costing you annually:

The premium

The deductible

The out-of-pocket maximum

The prescriptions

The appointments you skipped

The imaging you delayed

The ER visit you prayed wouldn’t happen

Own the number. Then get angry about it.

Make noise. Call your representatives. Show up. Vote in every election — not just the presidential ones. The people deciding this are not personally exposed to the consequences. They need to hear from the people who are.

Talk about it. The silence around healthcare costs is part of what keeps the system in place. When people don’t say what they’re actually paying, nobody knows how broken it really is.

Say it out loud.

Part II: Follow the Money. It Goes Somewhere Ugly.

This is Part I of a three-part series — The Gap — on what it costs to be in the middle in America right now.

Part II — Follow the Money. Who voted against Medicaid expansion. When. What their top donor industries are. The lobbying dollars flowing between the insurance industry and the people writing healthcare policy. All public record. All traceable. Side by side. No spin required.

Part III — The Rebuild. Three options. Real tradeoffs. What would actually fix it and what it would cost to get there.

The system is not broken.

It is working exactly as designed.

The only question left is whether we are willing to change who it works for.

The Jenn Files covers business, money, resilience, and grit — cutting through the noise so you can build something that can’t be broken. If this hit something, subscribe. Share it with someone who needs to read it. And if you want to go deeper, become a paid subscriber — the work that goes into this publication depends on your support.

Sources:

Insurance industry lobbying spend $183M in 2024: OpenSecrets.org

Premium comparison data: stridehealth.com, March 2026, unsubsidized rates, female, non-tobacco, income $63,000

Age rating: ACA allows insurers to charge older enrollees up to 3x younger enrollee rates

Premiums up 21% year over year: ValuePenguin, January 2026; CMS data

Six largest health insurance CEOs combined $159.4M in 2024: Fierce Healthcare, May 2025

CEO compensation ratios: Becker’s Payer Issues, SEC proxy filings, April 2025

Congressional salary $174,000 base: public record

Congressional health insurance taxpayer subsidy 72–75%: OPM, Congress.gov, No Labels, December 2025

US foreign aid FY2024: USAFacts, ForeignAssistance.gov

Israel $6.82 billion FY2024: USAFacts

Jordan $1.75 billion FY2024: Al Majalla, ForeignAssistance.gov

Total US aid to Israel since 1951, $317 billion inflation-adjusted: USAFacts; CFR

Israel universal healthcare: Commonwealth Fund International Health Policy Center

Jordan national health insurance: WHO Universal Health Coverage Partnership

G7 universal coverage: Commonwealth Fund Mirror Mirror 2024

Susie Wiles background: Britannica, Wikipedia, OpenSecrets

Susie Wiles breast cancer diagnosis: White House announcement, NBC News, March 17, 2026

10 states have not expanded Medicaid as of 2026: KFF State Health Facts

Enhanced ACA subsidies expired December 31, 2025: Center on Budget and Policy Priorities